New Delhi: It is that time of the year when one has to make a call whether to opt for the old tax regime or the new one. Filing income tax returns is a significant financial obligation for individuals, and understanding the different tax regimes is crucial for accurate reporting. With the introduction of the new tax regime in the Union Budget 2020, taxpayers have been presented with an alternative to the existing old tax regime.

The new tax regime promises lower tax rates but comes with a trade-off: removing several exemptions and deductions. The government has given the option to the taxpayers to choose between the old and new tax regimes.

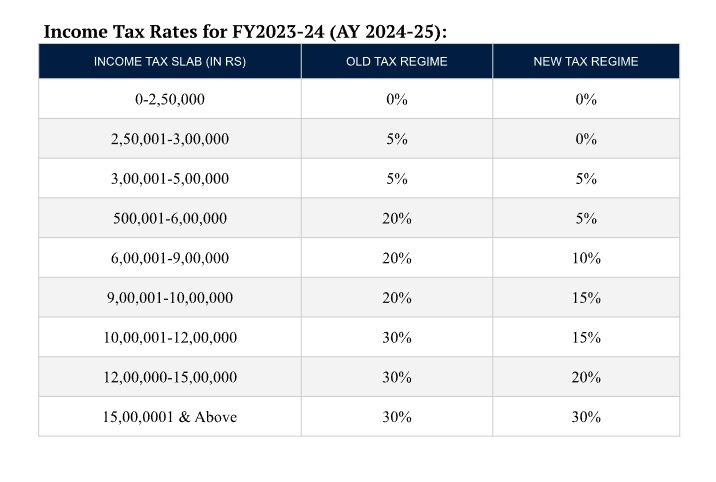

New Tax Regime

On February 1, 2020, Finance Minister Nirmala Sitharaman presented the Budget 2020, which included significant announcements, including introducing the New Tax Regime. Introducing the new tax regime aimed to simplify the tax structure and reduce the compliance burden on taxpayers. The key distinction between the two tax regimes lies in the income tax slab rates and the eligibility to claim exemptions and deductions.

The new regime disallowed several exemptions and deductions, such as HRA, LTA, 80C, 80D and more. To promote the new regime, the Union Budget for 2023-24 brought about revisions to the tax slabs specifically for the new regime, along with other changes. These changes are as follows:

Higher Tax Rebate Limit: The new tax regime now offers a total tax rebate on income up to ₹ seven lakhs, a significant increase from the Rs 5 lakh threshold in the old tax regime. This means that taxpayers with an income of up to ₹ seven lakhs will be completely exempt from paying any tax under the new tax regime.

Streamlined Tax Slabs: The tax exemption limit has been raised to ₹ three lakhs, although specific details regarding the new tax slabs were not provided in the given information.

These changes seek to make the new tax regime more appealing to taxpayers by providing increased benefits and simplifying the tax structure.

Old Tax Regime

The old tax regime refers to the tax system that was in place prior to the introduction of the new tax regime. In the old regime, taxpayers can access a wide range of exemptions and deductions, totalling more than 70. These include popular deductions like HRA (House Rent Allowance) and LTA (Leave Travel Allowance), which can reduce taxable income and lower tax payments.

One of the most significant deductions available in the old tax regime is Section 80C, which allows taxpayers to reduce their taxable income by up to Rs.1.5 lakh. This deduction encompasses various investments and expenses, such as contributions to the Employee Provident Fund, Public Provident Fund, life insurance premiums, and tuition fees.

Basic Exemption Limit

Under the new tax regime, the basic tax exemption limit will remain unchanged for all assesses, including senior citizens. This means opting for the new regime will not provide additional tax exemption for senior and super-senior citizens.

Enhancements and Changes in Tax Provisions

Standard Deduction: The standard deduction of Rs 50,000, previously available only under the old tax regime, has also been extended to the new tax regime. This means taxpayers can claim a standard deduction of Rs 50,000 from their salary income, reducing their taxable income. Under the new regime, along with other deductions and rebates, this can result in a tax-free income of up to Rs 7.5 lakhs.

Family Pension Deduction: Individuals receiving family pensions can claim a deduction of either Rs 15,000 or 1/3rd of the pension amount, whichever is lower. This deduction helps in reducing the taxable portion of the family pension received.

Reduced Surcharge for High Net Worth Individuals: For high net worth individuals with income exceeding Rs 5 crores, the surcharge rate has been reduced from 37% to 25%. This reduction in surcharge brings down their effective tax rate from 42.74% to 39%, providing some relief to individuals in this income bracket.

Higher Leave Encashment Exemption: The exemption limit for leave encashment has been raised for non-government employees. Previously set at Rs 3 lakhs, it has now been increased to Rs25 lakhs, resulting in an eight-fold increase. This higher exemption limit allows non-government employees to enjoy tax benefits on a more significant portion of their leave encashment amount.

Default Regime: Starting from the financial year 2023-24, the new income tax regime will be set as the default option. If taxpayers wish to continue using the old regime, they must submit a form when filing their tax return. Taxpayers can switch between the two regimes annually based on their circumstances and tax-saving preferences.

Changes in Deductions and Exemptions under the New Tax Regime

The New Tax Regime brought significant changes to tax exemptions and deductions. Here is a breakdown of what deductions have been removed and what deductions are still covered under the New Tax Regime:

Deductions Not Covered in the New Tax Regime:

- Leave Travel Allowance

- House Rent Allowance

- Standard deduction of Rs 50,000 (available for salaried individuals until AY 2023-24)

- Deductions available under Section 80TTA/TTB

- Entertainment allowance deduction and professional tax (for government employees)

- Tax relief on interest paid on home loans for self-occupied or vacant property under section 24

- Retrenchment compensation

- Tax-saving investment deductions under Chapter VI-A (80C, 80D, 80E, 80CCC, 80CCD, 80DD, 80DDB, 80EE, 80EEA, 80EEB, 80G, 80GG, 80GGA, 80GGC, 80IA, 80-IAB, 80-IAC, 80-IB, 80-IBA) (Except for deduction under Section 80CCD(2), 80JJA, and 80CCH).

Deductions Covered in the New Tax Regime:

Income from Life Insurance

Money received as a scholarship for education, etc.

Leave encashment on retirement

Agricultural income

Standard Deduction on Rental Income and Standard Deduction of INR 50,000 for salaried individuals, pensioners, and INR 15,000 for family pensioners (AY 2024-25 onwards)

Deduction of INR 15,000 from family pension (until AY 2023-24)

VRS proceeds up to INR 5 lakhs

Death cum retirement benefit

Tax Calculation Comparison: Old vs. New Tax Regime

1. When total deductions are Rs 5 lakhs or less: In this case, the new tax regime will typically be more beneficial. The new regime offers lower tax rates, which can offset the absence of deductions and exemptions available in the old regime.

2. When total deductions are more than Rs 3.75 lakhs: If your total deductions exceed Rs 3.75 lakhs, opting for the old tax regime is likely more advantageous. The numerous deductions and exemptions in the old regime can significantly reduce your taxable income and lower your overall tax liability.

3. When deductions fall between Rs 1.5 lakhs to Rs 3.75 lakhs total: The decision between the old and new tax regimes becomes more nuanced in this scenario. It will depend on your income level, specific deductions, and exemptions you qualify for. Conducting a comprehensive tax calculation based on your individual circumstances is recommended to determine which regime is more favourable for you.

Difference Between Old Vs. New Tax Regime: Which is better?

Determining which tax regime, the old or the new, is better depends on individual circumstances and financial goals. Here are some key differences between the two regimes to consider:

Tax Rates: The new tax regime offers lower tax rates than the old regime. This can result in lower tax liabilities for individuals with higher income levels.

Exemptions and Deductions: The old regime allows for various exemptions and deductions, such as HRA, LTA, standard deduction, and deductions under Section 80C, 80D, etc. These deductions can significantly reduce taxable income. However, the new regime does not allow most exemptions and deductions, resulting in a simplified tax structure.

Simplicity and Compliance: The new tax regime aims to simplify the tax system and reduce compliance burdens. With fewer exemptions and deductions, taxpayers can experience a streamlined filing process.

Flexibility: Under the old regime, taxpayers can choose and claim applicable exemptions and deductions based on their financial situation. In contrast, the new regime offers a standardized tax structure without the need to track and claim various deductions.

Long-term Impact: The choice between the two regimes should also consider long-term tax planning. If the old regime provides significant tax savings through exemptions and deductions, it may be beneficial in the long run. On the other hand, the new regime’s lower tax rates could be advantageous for individuals with higher income levels.

Ultimately, deciding which tax regime is better depends on income level, available exemptions, deductions, and personal financial goals.