Technological advancements and startups share a mutually reinforcing relationship: the startups drive innovation by leveraging emerging technologies, while these technologies open new avenues for entrepreneurial ventures. Thus, technological advancements are catalysts that determine what the startups can achieve, often disrupting traditional business models and paving entirely a new way to business and developing new markets.

Entrepreneurial ventures are crucial in generating employment opportunities and promoting economic growth. Over the years, India has emerged as a formidable innovation and entrepreneurial growth player, challenging advanced economies like the United States. India is steering significant social and economic development with its thriving startup ecosystem and technological advancements.

The World Intellectual Property Organization’s (WIPO) report on the Innovation Index 2024 placed India at 39th among 133 global economies. India stood in the 81st position in 2015, rising to 39th in 2024, reflecting India’s focused approach towards nurturing innovation across the sectors. India, along with four other middle-income economies apart from China, are among the top 40 economies, namely Malaysia (33rd), Turkey (37th), Bulgaria (38th), and India (39th).

India continues leading as the longest-standing innovation outperformer for the 14th consecutive year. In 2023, global patent filings declined by 2% for the first time since the financial crisis in 2009. In 2023, international patent filings under the WIPO-administered Patent Cooperation Treaty (PCT) fell by almost 2 per cent. This marked the first decline since the financial crisis in 2009. Similarly, advanced countries like the United States and Japan experienced a steeper decline of 5.3% and 2.9%, respectively. In contrast, India showed substantial growth; the PCT applications reported an impressive 44.6 per cent growth.

Typically, start-ups are newly established businesses or extensions of existing enterprises with novel or innovative business propositions. Entrepreneurs establish startups to develop innovative products, services, or business models. Today, the startup ecosystem is experiencing profound shifts characterised by growth opportunities and challenges. The growth opportunities originate from Artificial Intelligence. Enterprises are integrating artificial intelligence (AI) with their processes to improve safety, quality, and functionality of products and services.

In 2023, almost $40 billion was invested in Artificial Intelligence worldwide, emphasising AI's transformative potential and value proposition to businesses. Recent reports show that there are 67,200 artificial intelligence companies worldwide, of which 25% are AI companies and startups are based in the United States alone.

Of course, the AI ecosystem in India is evolving and developing at a fast pace. Today, India accounts for approximately 1,67,000 recognised startups, of which 6,636 are AI startups. AI startups account for only 4% of total startups, with an investment of over ₹one lakh crores, with steady growth.

In India, startups in the healthcare technology sector also witnessed tremendous growth with distinct services like telemedicine, personalised healthcare, and digitising health records, thus effectively transforming patient care and healthcare delivery. As per the reports, over 12,000 startups are functioning in the healthcare technology area.

India has been a leader in the FinTech landscape, with numerous companies and products. The FinTech industry continues to grow faster, solidifying its position as a global leader. The total market value of India's fintech companies is almost $ 90 billion, with over 26 fintech unicorns and one decacorn. The number of fintech startups in India has grown five times in the past three years, from 2,100 in 2021 to 10,200 in 2024.

The good news is that entrepreneurs are also focusing on developing solutions for environmental sustainability, including renewable energy, waste reduction, and sustainable urban development.

Though the startup growth story has been impressive so far, many struggle with several challenges to sustain their businesses. As a result of ongoing geopolitical tensions, the global startup ecosystem has been steering through tough times. The scarcity of funding opportunities has always constrained startups in every country, and India is no exception.

For example, venture capital funding declined from $ 530 billion in 2022 to $ 340 billion in 2023. The Asia-Pacific region has experienced a steep decline of over 40% in venture capital funding during the same period, reaching the lowest in the past nine years. However, Indian startups are exhorting remarkable resilience amid global economic uncertainties with a sizeable flow in venture capital funding. Despite the global slowdown, India's startup growth is undismayed, thanks to a series of strong and promising startups that continue attracting venture capitalists' investments.

Today opportunities are emerging for some startups, while many continue to face challenges in an environment where a slowdown cripples the economies. Many countries, including India, have been fighting high inflation and interest rates, thus creating challenges for startups. Another important area of concern for startups is regulatory compliance and continuous scrutiny. Sectors like fintech and data privacy are subject to stringent compliance norms, of course, in the larger interest of society.

The startups are also subject to intense competition in each marketplace. In India, where the markets are mature and well-developed, startups face competition. They always struggle to find ways to differentiate their product and services and compete in the marketplace. Thus, customer acquisition becomes more challenging.

The US has always been a global leader, with technology hubs like Silicon Valley, New York, and Australia contributing to technological innovation, fintech and healthcare technology, and Artificial Intelligence. Similarly, cities like London, Berlin, and Paris are well-known for fintech, AI, and sustainability startups.

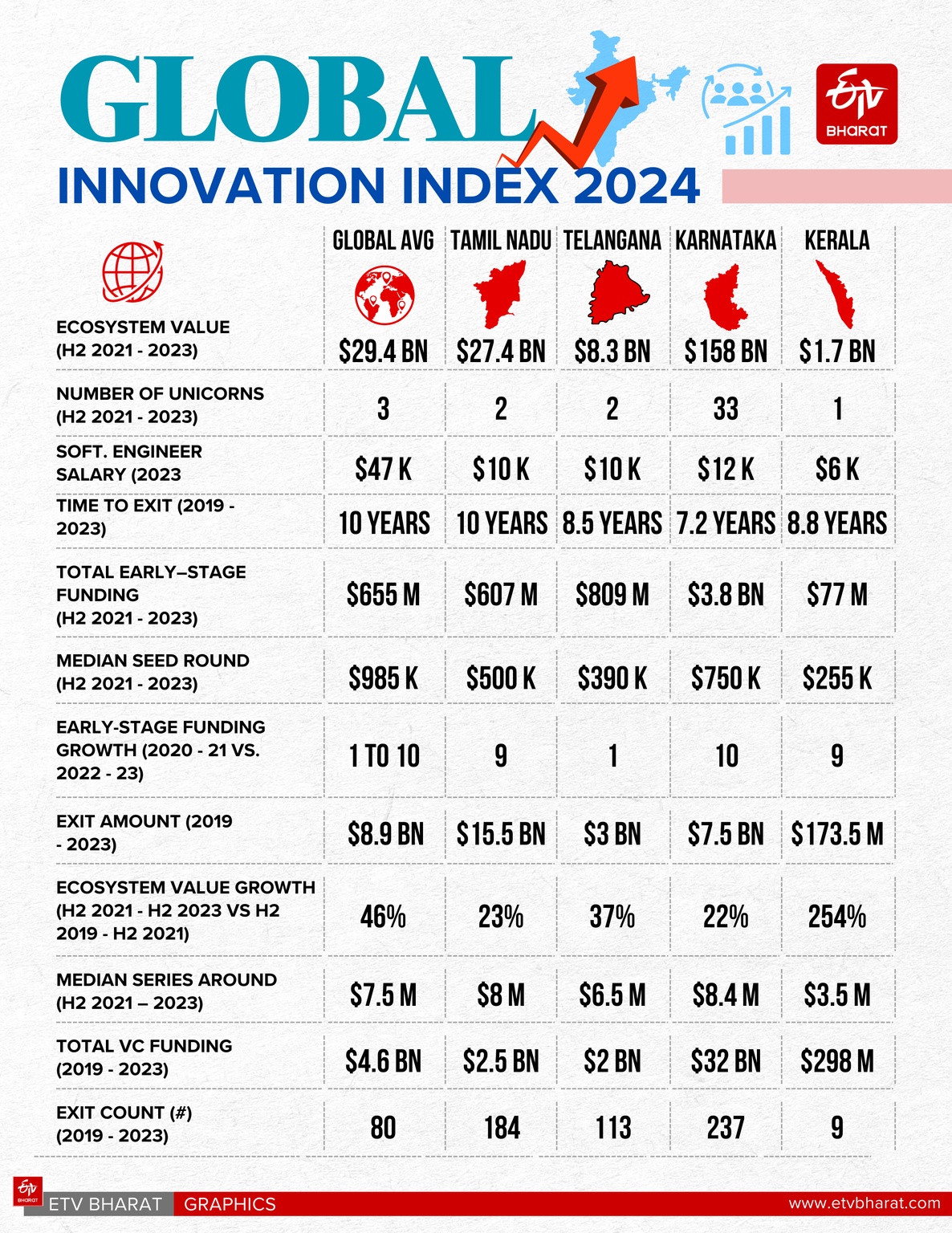

India’s startup ecosystem is the third largest in the world, with a strong focus on fintech, edtech, and Software as a Service (Saas). Bengaluru is considered the Silicon Valley of India, but it is far from Silicon Valley in the US in terms of size, number, employment, institutions, and impact on economic development. Though Bengaluru tops the list of startups in India with 1876, Delhi's capital region houses 1554, Mumbai is in third place with 1044, and Chennai and Hyderabad account for only 198 and 180, respectively.

The Bengaluru startup ecosystem dropped by one rank from 20th in 2023 to 21st in 2024, per the Global Ecosystem Report 2024. The other important cities in India, Delhi and Mumbai, are ranked 24th and 37th, respectively.

Hyderabad emerged as a technology hub due to the unwavering efforts of then Chief Minister Chandrababu Naidu in the late 1990s to early 2000s and has shown steady growth over the past twenty-five years. Today, Hyderabad is considered a contender in the startup race against other cities and ranked 41 and 50 under the emerging ecosystem category.

The present government should address the constraints holding back Hyderabad to be at the forefront of the technology and startup ecosystem. The government should also encourage a public-private partnership (PPP) model; for example, a rocket manufacturing startup in Hyderabad is a good beginning in the PPP model.

Though the growth of the Indian startup ecosystem has been healthy and impressive, it is far from that of other countries like the United States, Japan, etc. The government should focus on three areas to improve the startup ecosystem and its impact on the overall economy.

The first initiative should simplify regulatory compliance and eliminate bureaucratic hurdles. The second important area is improving infrastructure in cities with new-age business houses. The third and most important is training and skill development, which is complex and difficult to achieve. Finally, the government may establish exclusive financial institutions for startups in the PPP model.

(Disclaimer: The opinions expressed in this article are those of the writer. The facts and opinions expressed here do not reflect the views of ETV Bharat)